First-Time Homebuyer Closing Costs in Fairfax County: What to Budget Beyond Your Down Payment

- Johnny Sarkis

- Feb 19

- 8 min read

Why This Matters Right Now

You are deciding between renting and buying in a market that has cooled just enough to give you leverage. Local MLS data shows a median sale price near $682,500 with homes taking about 55 days to sell, which means more room for negotiation on closing cost credits. Meanwhile average rent around $2,300 to $2,600 per month keeps rising slowly, and mortgage rates are hovering near 7 percent. If you plan to buy a house, your upfront budget goes beyond the down payment. You need a clear line-item estimate of closing costs, prepaids, and reserves, so you can compare apples to apples against renting. The right plan helps you use seller concessions, down payment assistance, and smart negotiation strategies to reduce cash due at closing and tilt the rent vs buy math in your favor.

What You Need to Know Before You Compare Rent vs Buy

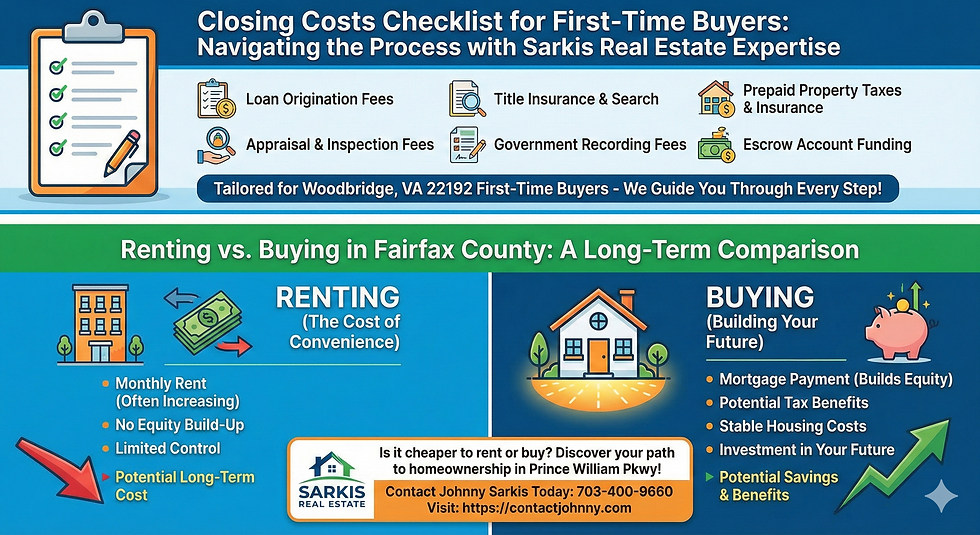

You face two types of cash outlays when you buy a house in Fairfax County: one-time closing costs and ongoing ownership costs. You should plan for both.

Closing costs typically total 2 to 5 percent of the purchase price

Prepaids include property taxes, homeowners insurance, and prepaid interest

Ongoing costs include mortgage, HOA fees, utilities, and maintenance

Typical closing cost line items in Northern Virginia:

Lender fees: origination, underwriting, processing, and credit report

Discount points or a temporary rate buydown if you choose to lower your rate

Appraisal: often $500 to $900 depending on property type and loan

Title services: title search, settlement fee, lender’s title policy, owner’s title insurance

Government charges: recording fees, recordation and intangible taxes on the loan

Escrow deposits: 2 to 6 months of property taxes and 2 to 3 months of insurance

HOA or condo costs: resale package, transfer fees, capital contribution, move-in fees

Property taxes and HOA fees are part of your real carrying cost. Fairfax County’s effective property tax rate is roughly 1.1 percent of assessed value, and HOA dues in many communities average about $195 to $326 per month. HUD fair market rent data and county income guidelines help you benchmark affordability if you are weighing rent to own paths, ADU or WDU options, or down payment assistance. As a first time home buyer, you can also explore county programs that allow as little as 2 percent down with credit score requirements typically starting around 620.

What 2 to 5 Percent Looks Like At Common Price Points

$400,000 purchase: closing costs roughly $8,000 to $20,000

$682,500 purchase: closing costs roughly $13,650 to $34,125

$765,000 purchase: closing costs roughly $15,300 to $38,250

These ranges include lender and title charges, government fees, and typical prepaids. Actual amounts vary by loan type, rate, HOA charges, and timing within the tax cycle.

How to Compare Your Options

You compare rent vs buy by looking beyond the monthly mortgage payment. Your monthly owner cost includes principal and interest, property taxes, homeowners insurance, HOA dues, and any private mortgage insurance if you put less than 20 percent down. In today’s market a conventional 20 percent down payment on a $765,000 home is large, so you might consider 3 to 10 percent down and use a seller credit to cover some closing costs. Your cash flow may be higher than renting at first, but you build home equity through principal paydown and potential price appreciation. County assessments rose in 2025, and local sales show steady long-run appreciation even with recent cooling.

Use a simple break-even test. Compare:

Renting at $2,300 to $2,600 per month

Owning at your projected monthly total plus upfront closing costs

Factor tax benefits of mortgage interest and property tax deductions

Add a conservative appreciation rate and rent inflation

Many Fairfax scenarios break even in 6 to 9 years when you include equity build and typical appreciation, especially if you secure seller concessions. If you prefer flexibility, renting may win in the first few years. If you value stability, school district ratings, and long-term wealth building, owning becomes compelling once you pass your break-even horizon.

Key factors to evaluate:

Time horizon: You gain the most if you hold 6 to 9 years or longer

Total monthly cost: Mortgage, taxes, insurance, HOA, and maintenance

Upfront cash: Down payment, closing costs, and reserves

Seller credits: 3 to 6 percent concessions can offset closing costs

Loan type: VA loan, FHA loan, conventional loan, jumbo loan affect costs

Rate strategy: Compare par rate vs discount points or a temporary buydown

Your Step-by-Step Guide

1) Get a mortgage pre-approval You should complete a full mortgage pre-approval to lock in a realistic price range. This sets expectations for interest rates, private mortgage insurance, and whether you need a seller credit to cover closing costs.

2) Price your monthly comfort zone You set a target payment that fits your debt to income ratio. Include taxes, insurance, HOA fees, and a maintenance reserve. Ask for itemized lender estimates so you can compare apples to apples across loan programs.

3) Request three lender quotes You compare rate, discount points, and zero point options. Review lender fees line by line. Ask for a temporary rate buydown option and a version with a seller-paid closing cost credit.

4) Shop title and settlement You can choose your title company. Compare settlement fee, title search cost, and owner’s title insurance. Title premiums are regulated, but total fees vary. Ask for a clear estimate that includes recording and transfer charges.

5) Estimate prepaids and escrows You prepay one year of homeowners insurance plus 2 to 3 months in escrow. You also prepay interest from closing date to month end. For taxes, budget 2 to 6 months escrow depending on the tax calendar and closing date.

6) Analyze HOA or condo charges You request the resale package early. Budget for transfer fees, capital contribution, and move-in fees. These can range from a few hundred dollars to over a thousand depending on the community.

7) Use market conditions to negotiate With days on market around 55 and a more balanced climate, you can ask for seller concessions. Depending on your loan, you can often request 3 to 6 percent in seller credits, which can cover a large share of closing costs.

8) Stack assistance programs You explore down payment assistance. Fairfax County programs have offered $10,000 to $20,000 on select developments and homebuyer initiatives, subject to eligibility, AMI limits, and program availability. You use assistance to reduce your down payment or cover part of your closing costs.

9) Finalize your offer strategy You set your offer price and decide on a closing cost credit vs a rate buydown. In a buyer’s market or on properties with longer days on market, you aim for a larger seller credit. In multiple offers, you prioritize price and appraisal strength.

10) Lock the loan and monitor fees You confirm your closing date, lock your rate, and request an updated loan estimate. Before your final walkthrough, review the closing disclosure to verify every line item.

What This Looks Like NearWoodbridge Va 22192

You may live or work near Woodbridge while shopping for homes for sale in Fairfax County. You benefit from strong commuter access via I-95, I-66, the Beltway, Fairfax Connector, VRE, and the Silver Line serving Vienna, Tysons, Reston, and Dulles. Local MLS data shows a balanced market with condos and some attached homes softer than single family homes, which can open the door to seller credits, repair credits, or a closing cost credit.

Price context that shapes your closing budget:

Single family homes in Fairfax often trade near or above $1.2 million in premium areas

Attached homes commonly around the mid $500,000s

Condos around the low $400,000s depending on size and location

Typical HOA fees in the region range from roughly $195 to $326 per month, and property taxes sit near 1.1 percent of assessed value. If you target homes near strong school clusters and transit, you can preserve long-run value and shorten your break-even. Neighborhoods that fit different budgets include Fairfax City areas close to George Mason, parts of Vienna with townhomes offering good square footage and garage parking, and Reston condos near the Silver Line that keep commute time in check.

Neighborhoods to consider:

Reston Town Center area condos: Great for walkability, mixed-use amenities, strong rental demand for future investment property potential, and pricing that keeps closing costs more manageable

Vienna townhomes near Metro: Solid school district ratings and convenient public transportation with price points that support seller credit negotiations

Fairfax City communities near George Mason: Starter condos and townhomes with lower HOA fees, quick access to parks and recreation, and a path to build home equity

What Most People Get Wrong

You might underestimate prepaids and escrows. Your lender controls impounds for taxes and insurance, which can add thousands to cash due at closing depending on date and tax calendar. You may also assume the seller always pays transfer taxes or HOA fees, yet Virginia customs vary by county and by contract. You could skip a home inspection to save money, but a thorough home inspection with radon or pest inspection often yields repair credits that offset closing costs. Some buyers overpay for discount points that do not break even within their time horizon. You should model both a seller-paid closing cost credit and a temporary rate buydown to see which delivers the higher net benefit. Finally, you need to budget for homeowners insurance, a possible survey for boundary lines, and post-closing reserves, especially if you buy a fixer upper rather than a move-in ready house.

Frequently Asked Questions

What closing costs do you pay as a first time home buyer in Fairfax County?

You typically pay lender fees, appraisal, title and settlement fees, owner’s and lender’s title insurance, recording and loan taxes, prepaid interest, homeowners insurance, escrow deposits, and any HOA or condo transfer costs. Depending on your loan type, you can often use a seller credit to reduce many of these expenses.

How much cash do you need beyond your down payment?

You should budget 2 to 5 percent of the purchase price for closing costs plus prepaids. On a $682,500 home, that is roughly $13,650 to $34,125, plus your down payment and earnest money. If you secure seller concessions or down payment assistance, you can significantly cut the cash you need to bring to closing.

Can you roll closing costs into your mortgage?

You can sometimes roll certain costs into your mortgage through a lender credit in exchange for a slightly higher rate. Government-backed loans may also allow financing of specific fees. Many buyers negotiate a seller-paid closing cost credit up to program limits. Your real estate agent and lender will help you structure the package that meets underwriting rules.

Are property taxes and HOA fees part of closing costs?

You prepay property taxes and homeowners insurance into escrow, and you may prepay a portion of HOA dues, transfer fees, and capital contributions. These are not lender junk fees but real ownership costs that affect your monthly budget. Plan for 2 to 6 months of taxes and 2 to 3 months of insurance in escrow depending on your closing date.

How can you get the seller to pay your closing costs?

You target properties with longer days on market, inspect thoroughly, and request a seller credit in your offer. Conventional loans often allow 3 to 6 percent seller concessions depending on down payment, FHA allows up to 6 percent, and VA permits concessions plus allowable fees. In a buyer’s market, a well-crafted concession request can cover most closing costs.

The Bottom Line

You should plan for closing costs of 2 to 5 percent of the purchase price in Fairfax County plus prepaids for taxes and insurance. In today’s balanced market, you can frequently use a seller credit, rate buydown, or closing cost strategies to reduce cash at closing. When you compare rent vs buy, consider your time horizon, equity growth, tax benefits, and the impact of closing cost strategies. If you are likely to stay 6 to 9 years, buying often beats renting over time, especially when you negotiate effectively and stack available programs.

If you're ready to explore your options for first-time homebuyer closing costs in the Fairfax County and Woodbridge area, Johnny Sarkis at Sarkis Real Estate can walk you through the specifics for your situation.

703-400-9660 0225167755

Comments